Budgets Don't Execute Themselves: Goal-Setting Guide

CFO confidence is up, but macro uncertainty isn't going anywhere. Your budget is approved, now make it survive 2026's "year of two halves." A practical goal-setting framework, plus two free tools.

Three rounds of revisions. One heated debate about headcount. A Friday afternoon board approval.

Everyone exhales. The budget gets filed. And then, slowly, it stops mattering.

Three months later: “Are we on track?” Variance reports. Explanations. Nothing changes.

The problem is not the budget. It is what happens after approval.

The recommendation is simple: if you want execution, you must translate the budget into clear goals, explicit ownership, and a review cadence that forces real decisions. This article is about how finance leaders do that.

Why Goal Setting Matters More Than Ever in 2026

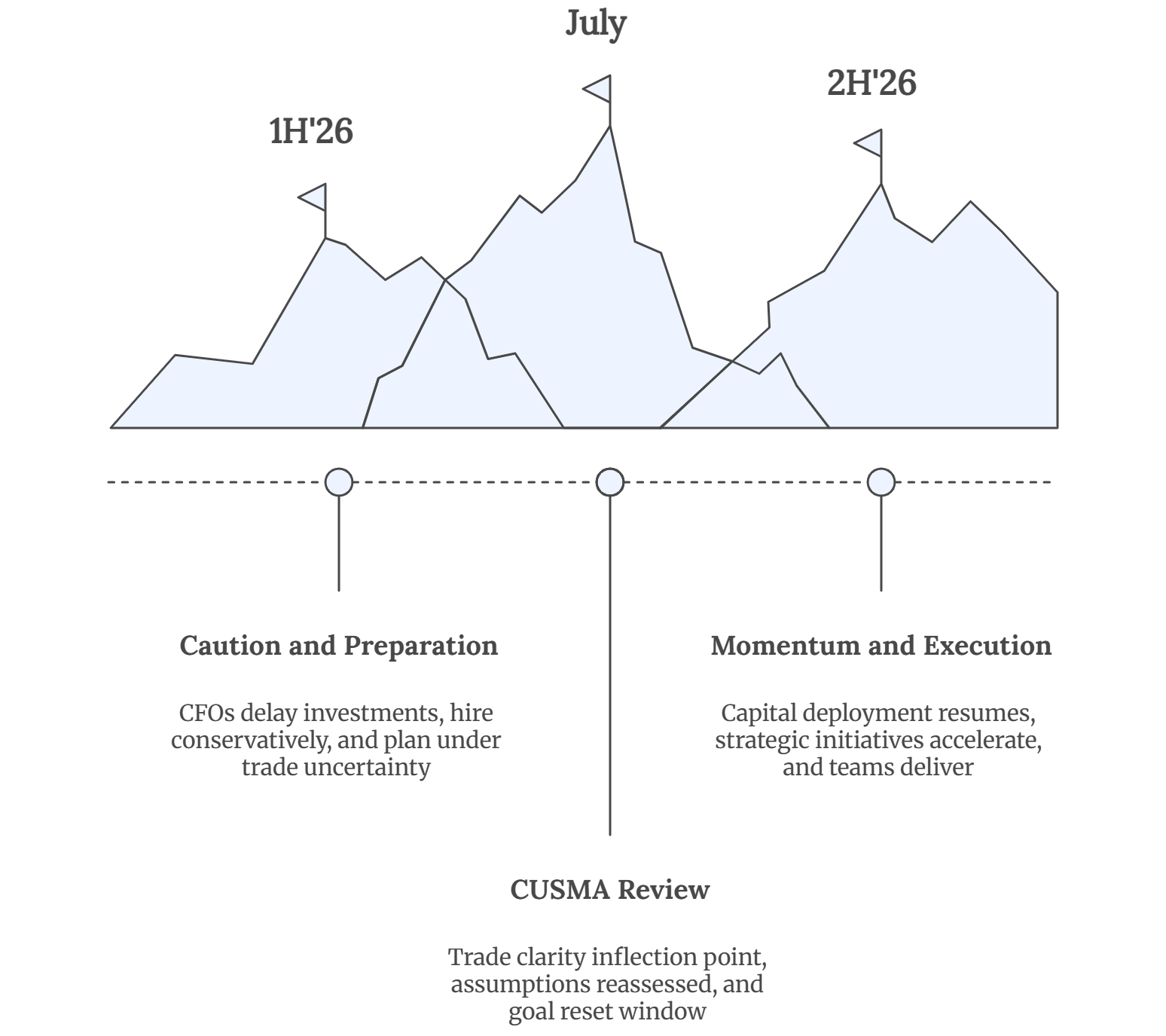

Deloitte Canada has framed 2026 as a “year of two halves.” The first half is expected to be cautious, with businesses delaying major decisions ahead of the July Canada-United States-Mexico Agreement (CUSMA) review. The second half is expected to move faster once there is clarity on trade conditions.

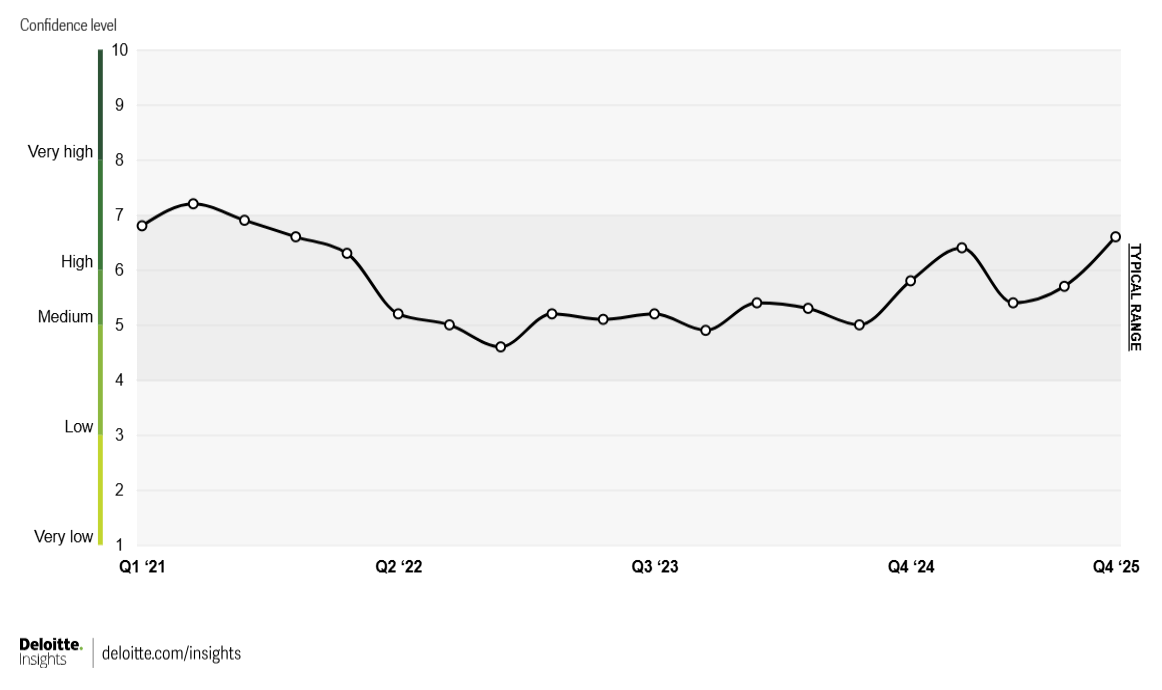

CFO sentiment is shifting in an important way.

According to Deloitte’s most recent CFO Signals survey, overall confidence has climbed into high territory for the first time in four years.

86% of finance leaders say they are more optimistic about their own company’s financial outlook than they were just one quarter ago.

What is interesting is where that optimism sits. While confidence in company prospects is high, confidence in the broader economy remains more muted.

Only about a third of leaders rate current economic conditions as good, even though more than half expect conditions to improve over the next year. Growth forecasts for revenue and earnings have softened slightly, even as confidence has risen.

Meanwhile, risk appetite is shifting quickly.

Nearly 60% of leaders now say this is a good time to take greater risks, almost double the level from six months earlier.

This gap between internal confidence and external uncertainty is exactly where traditional budgets break down. When conditions are unclear, static plans lose relevance, and execution depends less on annual numbers and more on how teams translate intent into action.

Put together, this paints a very specific picture. Leaders are not blindly optimistic about the macro environment. They are increasingly confident in what they can control inside their own companies, even while external uncertainty persists.

That tension matters.

In environments like this, many leadership teams default to waiting. Freeze hiring. Delay investments. Revisit decisions later. That instinct is understandable, but it often leads to something worse than making the wrong call. It leads to organizational drift.

What separates strong finance leaders in uncertain years is not prediction accuracy. It is preparation.

The finance leader who perform well in the second half of volatile years are rarely the ones who paused in the first. They are the ones who used the quieter period to tighten cost structures, improve operating discipline, build systems, and upskill teams.

Goals are how you do that without pretending you can see the future.

Why Budgets Fail

Most startup budgets fail in the same way.

They allocate dollars correctly, but they fail to drive behaviour.

A $200K line for automation does not tell anyone what success looks like. A headcount plan does not tell managers how to prioritize. A margin target does not tell teams which trade-offs matter.

Left alone, teams will optimize for what feels safe or visible. Hitting spend targets instead of improving outcomes. Deferring decisions to avoid missing the plan. Protecting budget instead of using it deliberately.

This is how budgets quietly become ceilings instead of enablers.

Goals are the mechanism that turns financial intent into operational focus.

Choosing the Right Goal Framework Without Overthinking It

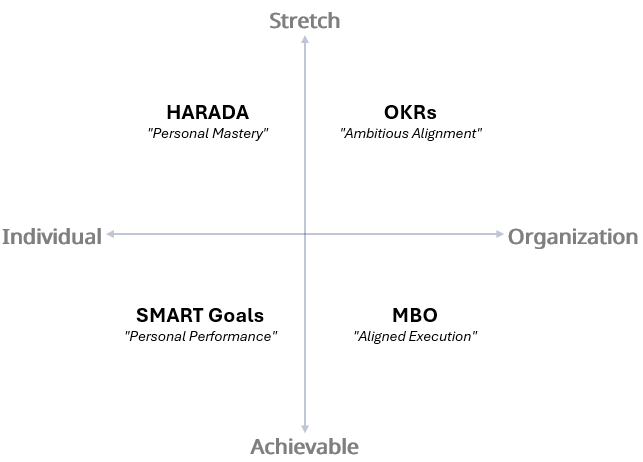

There are more goal setting frameworks than any finance leader needs. The mistake is treating them as interchangeable or trying to adopt several at once.

At a high level, frameworks differ on two dimensions. Individual versus organizational scope. Achievable targets versus stretch ambition.

SMART goals are criteria, not a system. They work well for individual accountability, performance management, and compensation alignment. Their limitation is that “achievable” often discourages ambition, and there is no built-in mechanism for alignment across teams.

Management by Objectives (MBO) can work in more traditional hierarchies, but in practice, they often devolve into annual goal-setting exercises that are revisited too infrequently to matter.

OKRs sit in the sweet spot for most startups. They create clarity between intent and measurement, encourage ambition, and scale across functions.

That is why they work. Not because they are trendy, but because they solve the coordination problem that budgets alone cannot.

How OKRs Actually Work in Practice

At their simplest, OKRs follow one formula.

“I will achieve this Objective as measured by these Key Results.”

Objectives are qualitative and directional. They answer what you are trying to achieve.

Key Results are quantitative and specific. They answer how you will know if you got there.

A common mistake is treating OKRs as glorified task lists. If your Key Results are activities like “implement system” or “hire analyst,” you are missing the point. Key Results should describe outcomes.

Another mistake is treating OKRs as commitments to hit 100%. Properly set OKRs are meant to be ambitious. Hitting roughly two-thirds of your Key Results usually means you set them correctly.

My Recommended Approach: Simplified OKRs

In early-stage companies, purity matters less than usability.

My approach is straightforward. Use OKRs as the structure, and use SMART criteria to validate Key Results.

Objectives stay aspirational. Key Results must be specific enough that there is no debate, measurable without heroic reporting, achievable but uncomfortable, relevant to the Objective, and time bound within the quarter.

This hybrid avoids vague ambition while preserving alignment.

It also maps cleanly to how leaders already operate. Quarterly OKRs align naturally with forecast updates, board cycles, and budget reviews.

For 2026 specifically, the “year of two halves” framing fits well. Use Q1 and Q2 to focus on what you can control. Treat July as a potential reset point. Adjust Q3 and Q4 with updated assumptions.

Translating a Budget Line Into a Real Goal

Let’s make this concrete.

Budget line: $200,000 allocated to finance automation tools.

Bad goal: Implement finance automation.

This tells you nothing about impact.

Better OKR

Objective: Eliminate manual work from the month-end close

Key Results:

Reduce the close cycle from twelve days to eight days by Q2

Automate three manual reconciliation processes by Q2

Zero overtime hours during the close week by Q3

This Budget to OKR Translator helps you get started if you’re stuck.

Now the spend has a purpose. The team knows what success looks like. Trade-offs become easier. If a tool does not move these metrics, it is the wrong tool.

This is the difference between budgeting and operating.

The Review Cadence Is Where Most Teams Fail

Setting goals is not the hard part. Reviewing them consistently is.

In practice, you need four distinct rhythms.

Weekly check-ins are tactical. Update confidence levels. Surface blockers. Adjust tactics, not goals.

Monthly reviews are cross-functional. Look for trends, capacity issues, and resource mismatches.

Quarterly grading and resets lock in learning and set the next quarter’s goals with intent.

Annual planning summarizes outcomes and sets direction, not detailed tasks.

If your weekly check-ins feel painful, that is useful information. It usually means goals are unclear, unmeasurable, or misaligned.

When to Change Goals and When Not To

One of the biggest fears leaders have about goal systems is rigidity.

The answer is not to change goals easily. It is to be explicit about when change is justified.

Legitimate reasons to change OKRs mid-cycle include black swan events, new information that invalidates your assumptions, or early discovery that a Key Result cannot be measured.

For Canadian companies in 2026, the July CUSMA review is a legitimate reset trigger. If trade conditions materially change, your assumptions change. Plan for that possibility explicitly.

This OKR Decision Tool helps you navigate mid-cycle goal changes.

Do not change goals because they are hard, you are behind, or someone dislikes their target. That is where the learning happens.

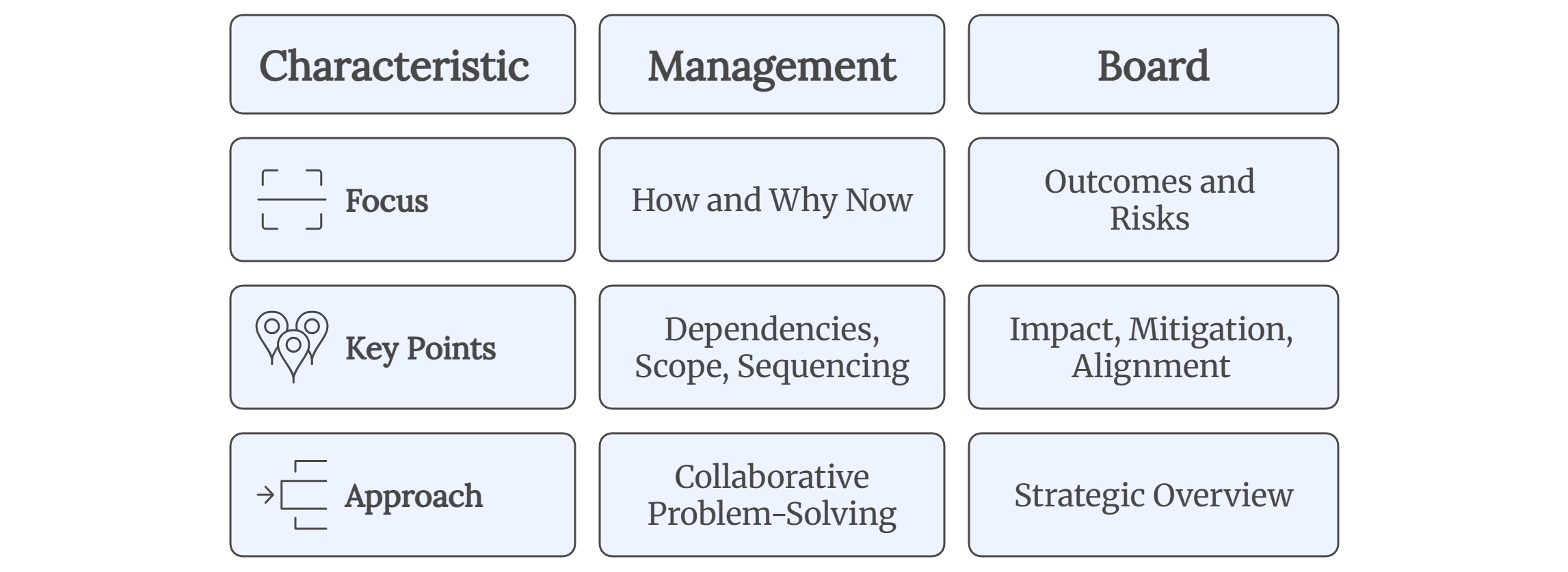

Discussing Goals With Management Versus the Board

The same goals should not be framed the same way to every audience.

With the management team, lead with why the goal matters now. Surface dependencies early. If Finance needs Engineering support to implement a billing system, say it explicitly. Negotiate scope and sequencing. Do not dictate.

With the board, elevate the conversation. Boards care about outcomes and risk, not tools and tasks. Reduce close cycle by 30% is more meaningful than implement a new system. Extend runway by two months lands better than save fifty thousand dollars.

In 2026, boards will be thinking about trade risk, whether you raise it or not. Frame early year goals as building optionality. Investments that pay off regardless of how July unfolds.

A Practical Q1 2026 Playbook

If you want to operationalize this quickly, here is a simple four-week plan.

Week one: Review the approved budget. Identify three to five initiatives that actually matter.

Week two: Draft one Objective per initiative. Define two to four measurable Key Results for each. Run them through the SMART filter.

Week three: Share draft OKRs with leadership peers. Identify dependencies. Adjust scope.

Week four: Schedule your first weekly check-in. Keep it short. Pick one blocker to remove.

Do not over engineer this. Momentum matters more than elegance.

Resolutions fade. Resets stick.

A budget without goals is just a spreadsheet. Goals without a review cadence are just wishes.

What is the one goal that, if you achieved it this quarter, would materially change your company’s trajectory? Hit reply, I’d love to hear it!

Start simple. Three objectives. Nine Key Results. Weekly check-ins.

Thanks for reading, until next time!

- Kunal